US GDP Grows 2.6% in Q3 Driven Entirely by Trade; Price Index Comes Cooler Than Expected

By: Tyler Durden

October 27, 2022: Ahead of today's GDP print, economist consensus was that in the 3rd quarter, the US economy would grow if entirely on the back of net exports (or trade), and sure enough that's precisely what happened. While the BEA reported that in the third quarter, US GDP rose 2.57%, more than the 2.4% consensus and up notably from last quarter's -0.6% and the -1.6% drop in Q1...

According to the BEA, the upturn in the third quarter, compared to the second quarter, primarily reflected a smaller decrease in private inventory investment, an upturn in government spending, and an acceleration in nonresidential fixed investment that were partly offset by a larger decrease in residential fixed investment and a deceleration in consumer spending. Imports turned down.

But, again, it was all about trade...

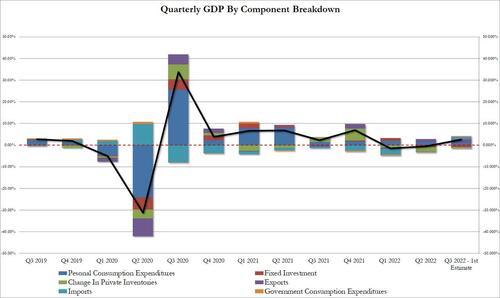

... as the following breakdown shows:

Personal Consumption: 0.97% of the bottom-line number, down from 1.38% and the lowest since 2019.

Fixed Investment subtracted -0.89% from the GDP, in line with last month's -0.92% as corporations continue to retrench ahead of the recession

The change in private inventories shrank for the 3rd quarter, this time shrinking GDP by -0.70%

On the positive side net exports rose by 2.77% courtesy of a 1.63% increase in exports and a decline in imports which contributed another 1.14% to the GDP print. As noted above, this alone was enough to explain the entire gain in Q3 GDP, and is a function of US support of the European war economy as the US exports record amount of commodities (oil and gas) as well as weapons to Europe.

Finally, government consumption - which was and remains an oxymoron - added 0.42% to the bottom-line GDP.

Looking at the slowdown in consumption, BBG notes that personal consumption expenditures on goods were down 1.2% annualized in Q3, after dropping 2.6% in Q2. Meanwhile, growth of personal consumption expenditures on services moderated to 2.8%, from 4.6%.

Commenting on the surge in trade, the BEA wrote that the increase in exports reflected both goods (led by industrial supplies and materials as well as nonautomotive capital goods) and services (led by “other” business services and travel). Some more details:

The increase in consumer spending reflected an increase in services (led by health care and "other" services) that was partly offset by a decrease in goods (led by motor vehicles and parts as well as food and beverages).

The increase in business investment reflected increases in equipment and intellectual property products that were partly offset by a decrease in structures.

The increase in government spending reflected increases in federal (led by defense spending) as well as state and local.

The decrease in housing investment was led by new single-family housing units and brokers’ commissions.

The decrease in private inventory investment was led by retail trade (mainly “other” retailers).

The decrease in imports reflected a decrease in goods (led by consumer goods) that was partly offset by an increase in services (led by travel).

And while the headline GDP was generally in line with expectations, where the market was decidedly pleased was to learn that the GDP price index rose just 4.1%, well below the 5.3% expected, and down more than half from 9.0% last quarter.

Excluding food and energy, core PCE 4.5% after increasing 4.7%, in line with expectations. This was enough to whiplash the USD, which was spiking after the somewhat dovish ECB (having dropped the "next several meetings" language), and reverse some of its gains in what has so far been a very fast, nail-bitting session.

Today data, according to some such as the FT, "ends a debate that raged over the summer as to whether the US economy was already in a recession" although we disagree since the only reason the GDP print was strong is because Europe is collapsing into a recession and is now overly reliant on US energy and weapons exports; the GDP print also did little to dispel fears that the US will eventually (again) tip into an even bigger recession given the aggressive steps the US central bank is taking to stamp out elevated inflation.

Two consecutive quarters of shrinking GDP has long been considered a common criterion for a so-called “technical recession”. However, top policymakers in the Biden administration and at the Federal Reserve pushed back forcefully on that framing, citing ample evidence that the economy was still on firm footing. The Fed is poised early next month to deliver its fourth consecutive 0.75 percentage point interest rate increase, which will lift its benchmark policy rate to a new target range of 3.75 per cent to 4 per cent. As recently as March, the federal funds rate hovered near zero, making this tightening campaign one of the most aggressive in the US central bank’s history.

As of last month, most officials thought the fed funds rate would peak at 4.6%, but now investors expect it to close in on 5% next year (that said, today's weaker than expected PCE print will likely ease those bets). Given how large an impact the Fed’s actions are expected to have on growth and the labour market, most economists now expect the unemployment rate to rise materially from its current level of 3.5 per cent and for the economy to tip into a recession next year.

Top officials in the Biden administration maintain that the US economy is strong enough to avoid that outcome, citing the resilience of the labor market, but even Jay Powell has acknowledged the odds have risen. “No one knows whether this process will lead to a recession or if so, how significant that recession would be,” he said at his last press conference in September.

Source: ZeroHedge